Chapter 3 ARIMA Models

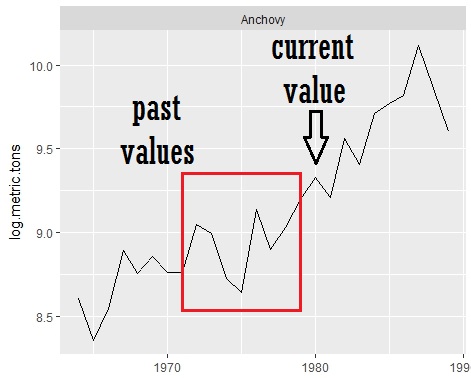

The basic idea in an ARMA model is that past values in the time series have information about the current state. An AR model, the first part of ARMA, models the current state as a linear function of past values:

\[x_t = \phi_1 x_{t-1} + \phi_2 x_{t-2} + ... + \phi_p x_{t-p} + e_t\]