Chapter 2 Time-varying regression

Time-varying regression is simply a linear regression where time is the explanatory variable:

\[log(catch) = \alpha + \beta t + \beta_2 t^2 + \dots + e_t\] The error term ( \(e_t\) ) was treated as an independent Normal error ( \(\sim N(0, \sigma)\) ) in Stergiou and Christou (1996). If that is not a reasonable assumption, then it is simple to fit a non-Gausian error model in R.

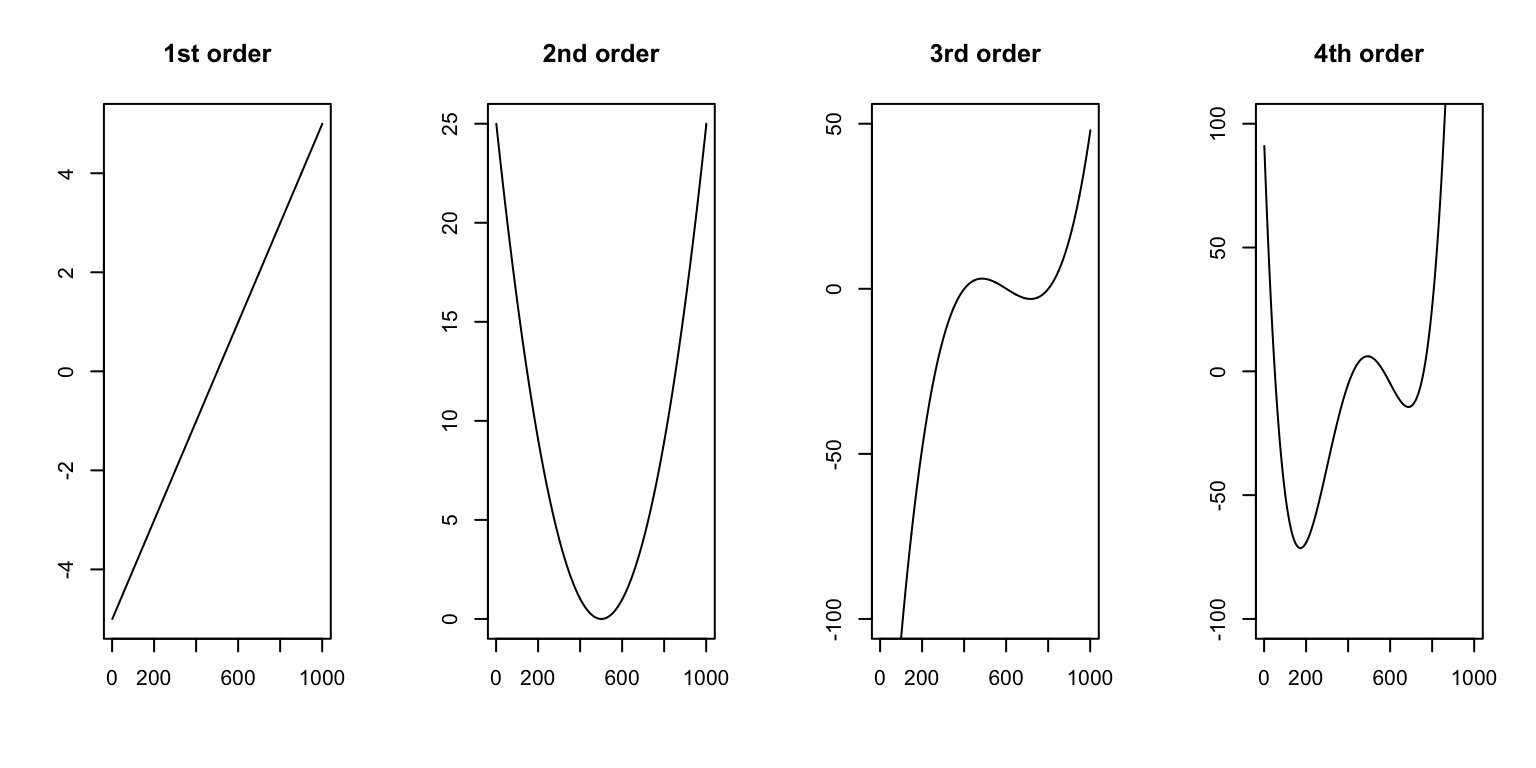

Order of the time polynomial

The order of the polynomial of \(t\) determines how the time axis (x-axis) relates to the overall trend in the data. A 1st order polynomial (\(\beta t\)) will allow a linear relationship only. A 2nd order polynomial(\(\beta_1 t + \beta_2 t^2\)) will allow a convex or concave relationship with one peak. 3rd and 4th orders will allow more flexible relationships with more peaks.